Beyond the hype and headlines, blockchain’s potential extends far beyond the world of digital currencies. Its promise of decentralization, immutability, and transparency has sparked change across industries, from finance and supply chain management to healthcare and telecommunication.

Amidst the excitement and allure, a crucial question emerges: Is blockchain truly the magic wand for every business? Or is it merely a shiny new tool better suited for specific tasks?

Understanding blockchain’s strengths

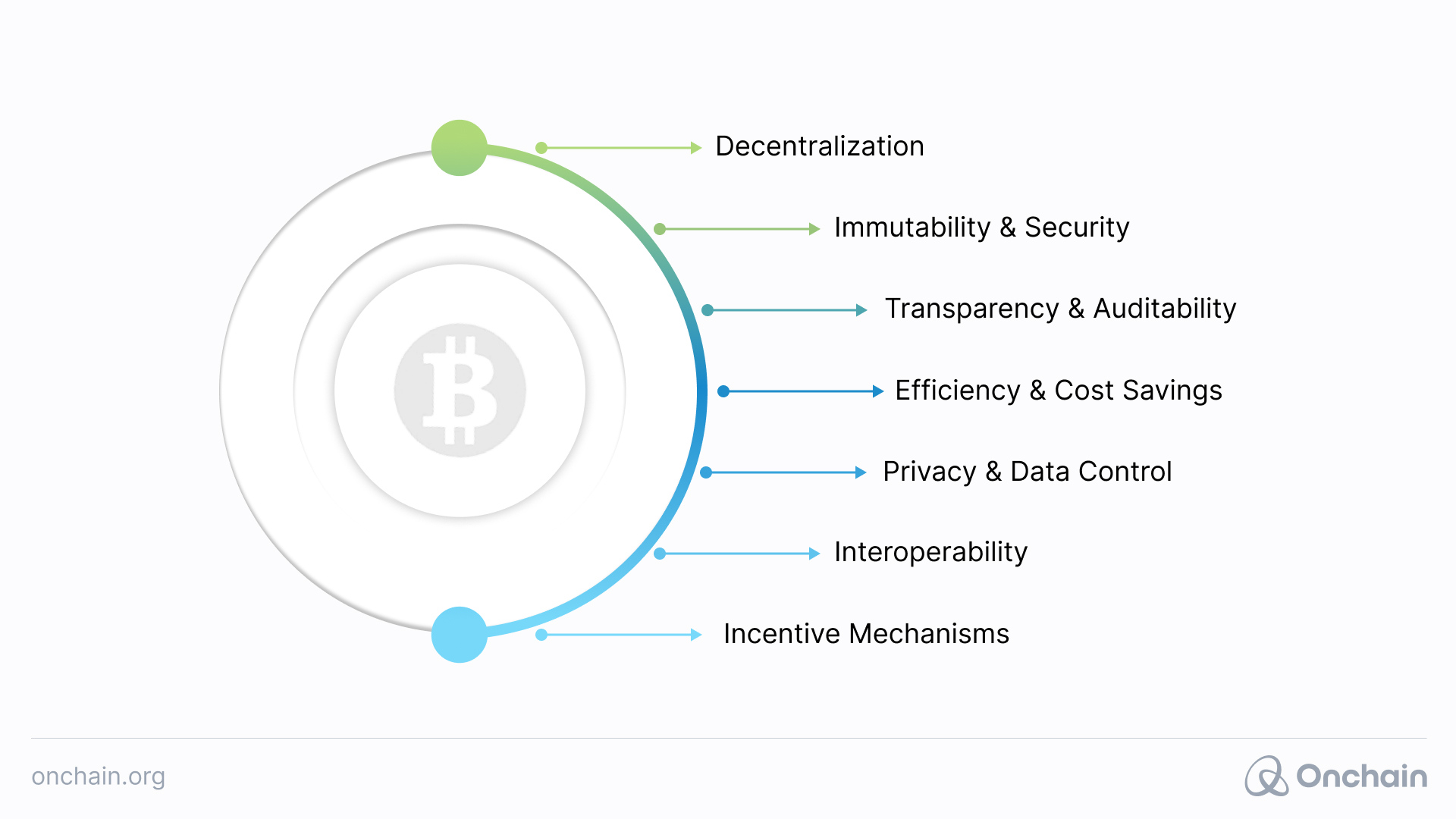

At its core, blockchain is a distributed ledger technology (DLT) that securely records transactions across multiple nodes or computers. Its decentralized nature eliminates the need for a central authority, offering several advantages:

These benefits showcase blockchain’s versatility, but understanding its strengths alone isn’t enough. To truly determine whether blockchain is beneficial for your business, it’s essential to examine the specific problems it solves.

What business-specific issues does it solve?

The financial sector was an early adopter of blockchain technology, drawn to its unparalleled security features. Soon, other industries realized its potential extended far beyond finance. It was like a Swiss Army knife with hidden tools, each solving a specific challenge. From authenticating diamonds to tracking coffee beans, blockchain quietly revolutionized industries, creating a more transparent and efficient world. And this is just the beginning.

Now that we understand what blockchain offers, let’s see how these strengths translate into real-world problem-solving.

1. Lack of trust and transparency:

In many industries, particularly those with complex supply chains or multi-party transactions, establishing trust and ensuring transparency can be major hurdles.

- Blockchain solution: Blockchain creates an immutable and shared ledger, providing transparency in every transaction. This shared visibility helps build trust among all participants.

- Example: Walmart uses blockchain to track the origin and journey of food products. This not only enables quicker identification of contaminated items but also improves food safety by providing transparent tracking for authorizers from farm to table.

2. Inefficient and costly processes:

Manual processes, intermediaries, and reconciliation errors are common inefficiencies that can drive up operational costs in many industries, such as energy trading, real estate records, insurance claims, etc.

- Blockchain solution: Through the use of smart contracts, blockchain automates processes, reducing the need for intermediaries and streamlining transactions. This results in cost savings and increased operational efficiency.

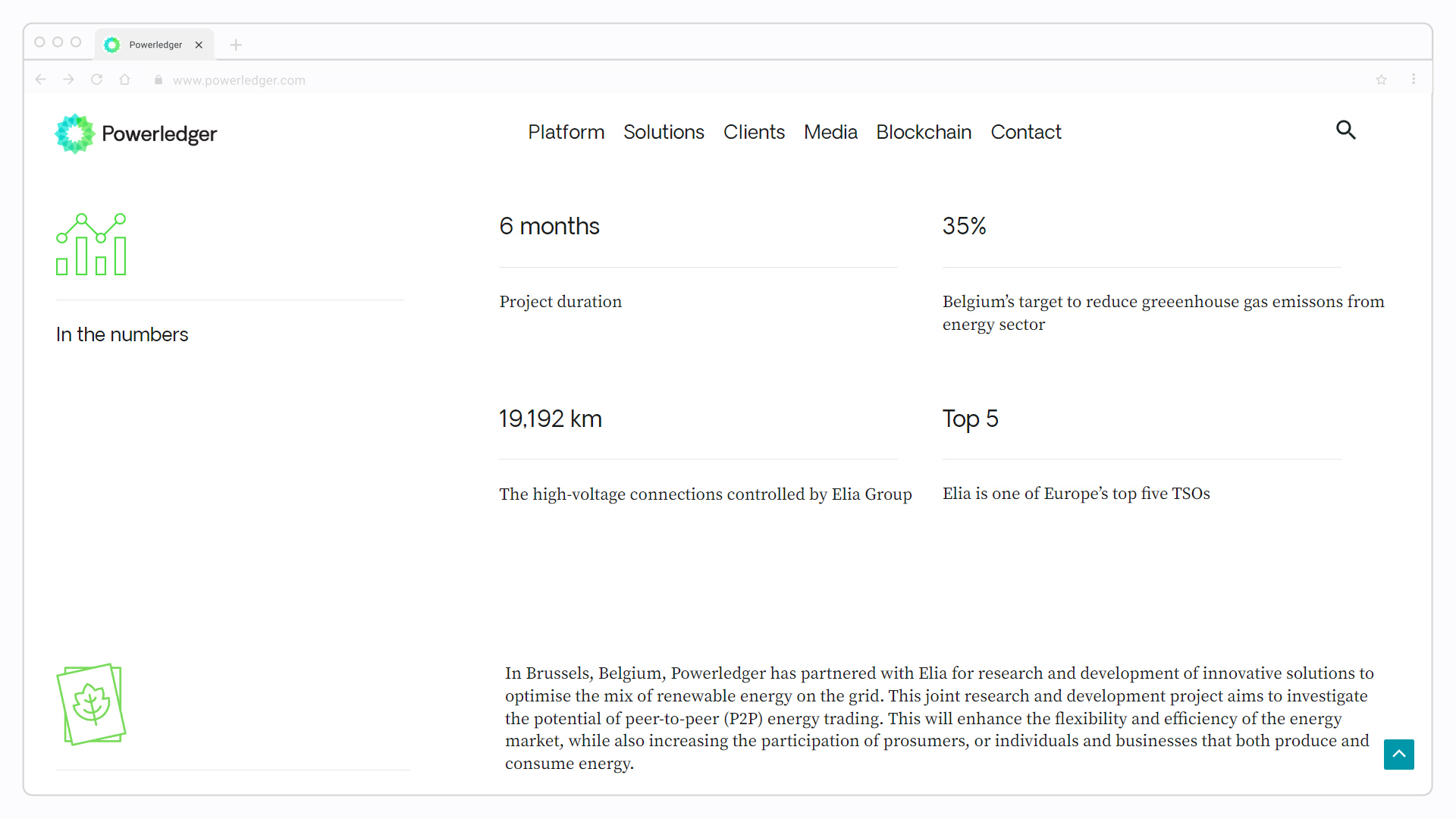

- Example: The blockchain-based energy trading platform Powerledger facilitates peer-to-peer energy trading in various communities around the world.

Many such projects in the DePIN sector are addressing global issues like climate change and solve real-world problems through blockchain integrations. Check out such integration details in our report on how DePIN brings real-world business opportunities for Web3.

3. Data security and privacy concerns:

In today’s digital world, data breaches and unauthorized access can lead to significant financial and reputational damage for businesses.

- Blockchain solution: Blockchain enhances data security by decentralizing and encrypting data, making it extremely difficult for hackers to tamper with information.

- Example: Medicalchain uses blockchain to securely store and share patient health records, ensuring privacy and giving patients control over their own data. Similarly, Solve.Care enables patients to securely manage their health information through blockchain technology.

4. Counterfeiting and fraud:

Counterfeit products and fraudulent activities not only cause financial losses but also tarnish the reputation of businesses.

- Blockchain solution: Blockchain creates a permanent and tamper-proof record of product authenticity, making it easier to track and verify goods, and significantly reducing counterfeiting and fraud.

- Example: Clarins, a skincare company, uses blockchain combined with machine learning to verify the authenticity of ingredients. This ensures that only genuine materials enter their supply chain.

- Check our report on more such use cases on AI x Blockchain.

5. Complex and slow cross-border payments:

Traditional cross-border payments are often slow, costly, and involve multiple intermediaries, leading to inefficiencies for businesses.

- Blockchain solution: Blockchain enables faster, cheaper, and more secure cross-border payments by bypassing traditional banking systems.

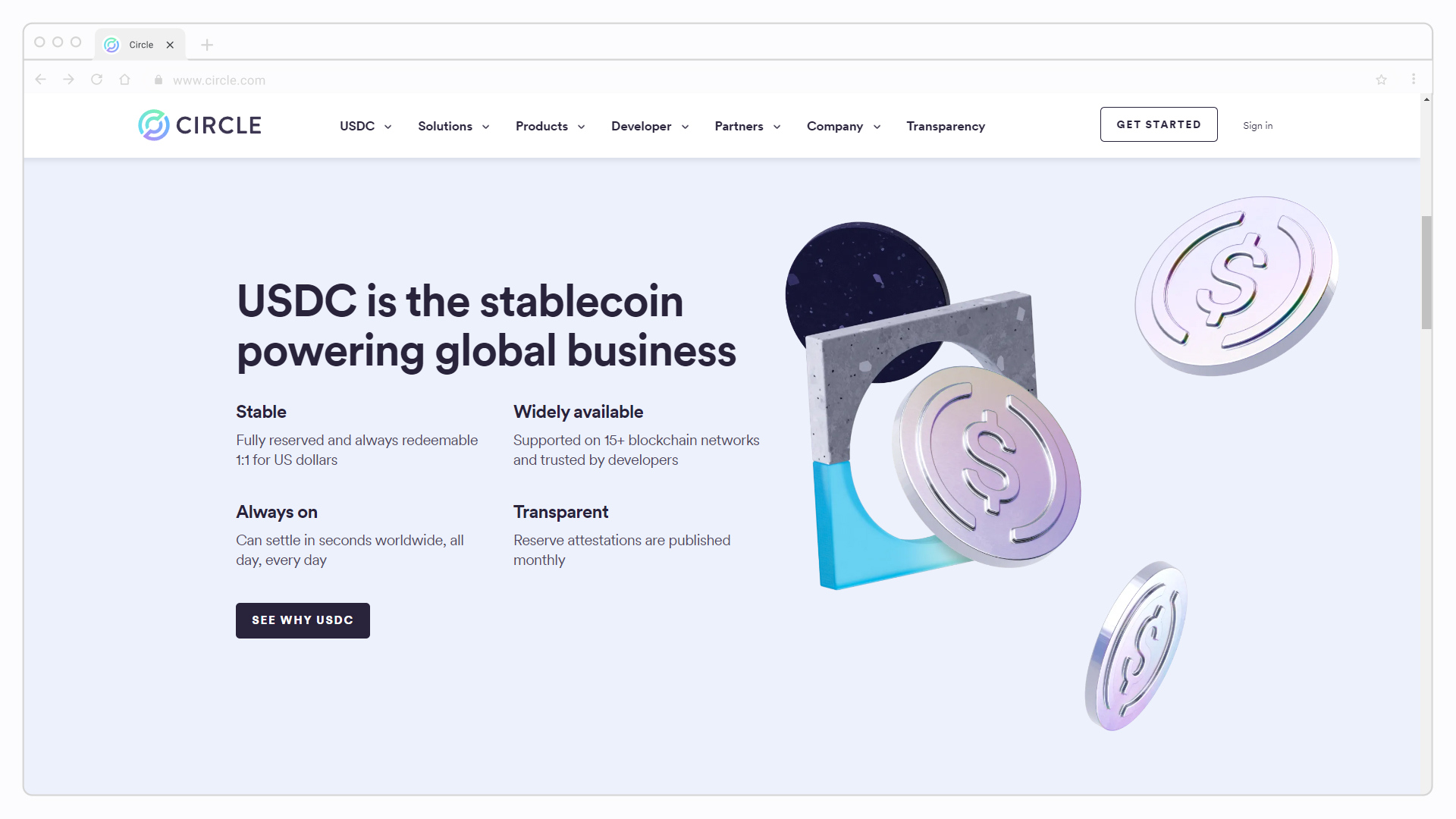

- Example: Ripple’s blockchain network allows financial institutions to facilitate real-time international payments, reducing both the cost and settlement times. Companies like Circle and Tether issue stablecoins that can be used for fast and efficient cross-border transactions, especially in regions with limited access to traditional banking systems.

The Onchain Research Team is currently working on a comprehensive stablecoin report that will delve deeper into this exciting application of blockchain technology, showcasing its potential to change the global payments landscape. Stay tuned for a detailed analysis of blockchain’s biggest business use case!

Do I really need to adopt blockchain for my business?

“Blockchain isn’t a one-size-fits-all solution.”

Blockchain may seem like a magic bullet, but it’s important to remember that it isn’t a one-size-fits-all solution. Just because blockchain can solve certain problems doesn’t mean it’s necessary for every business or use case.

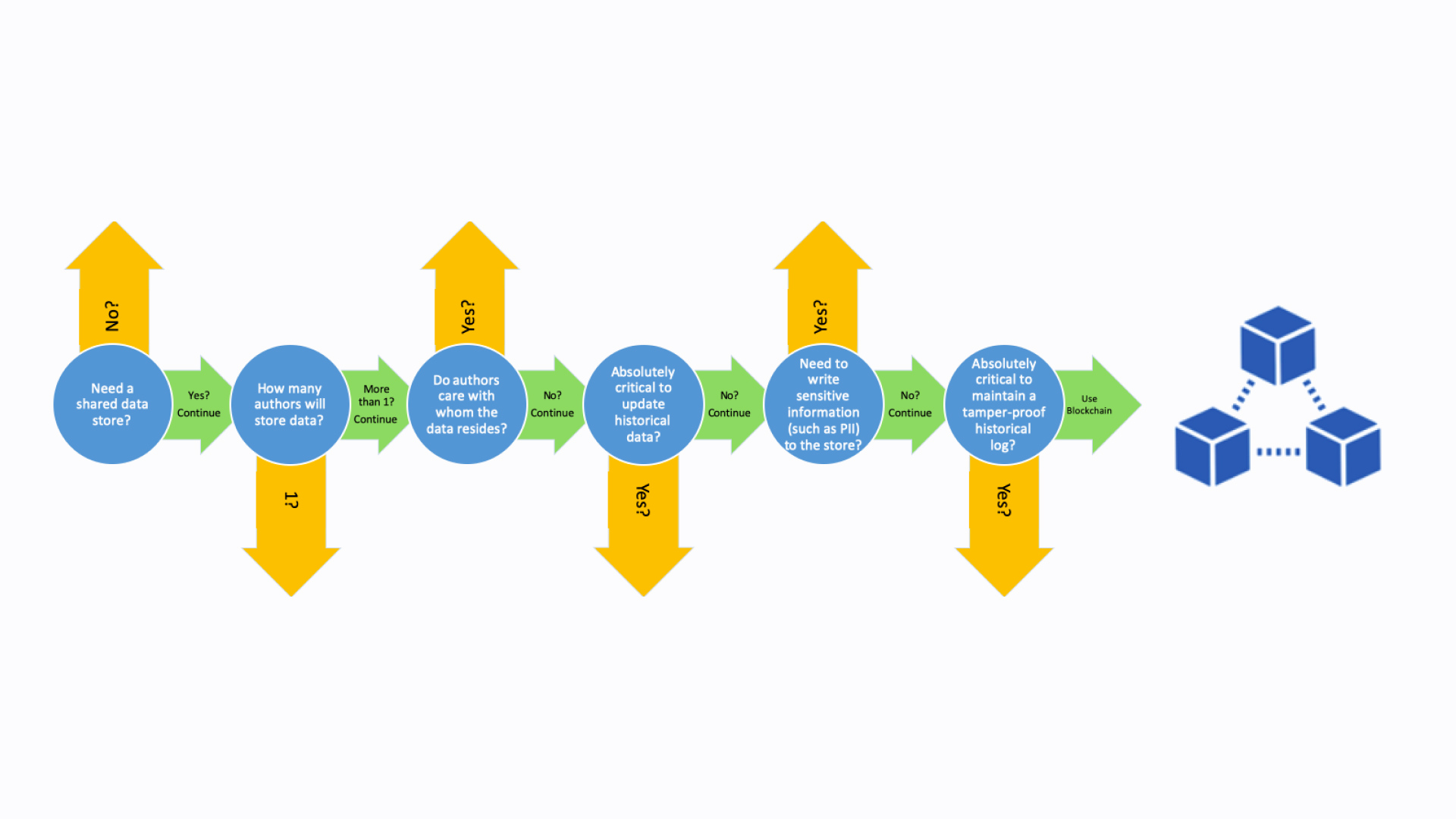

So how do you determine whether blockchain is essential for your business? Here’s a quick guide to help:

In a nutshell:

- No data to store? You don’t need blockchain. Stick to a simpler database.

- One writer only? Traditional databases will be faster and easier to manage.

- Trustworthy middleman? Let them handle updates—they might do the job without the complexities of blockchain.

- Need public transparency? A public blockchain may be the answer.

- Need privacy and control? Consider a permissioned blockchain where data access is restricted to approved members.

- Multiple parties involved, with trust issues? A permissionless blockchain could be the ideal solution, offering transparency to all participants.

Evaluating the alternatives

As discussed previously, before diving headfirst into blockchain-based solutions, it’s essential to consider alternative solutions that might offer similar benefits without the complexities.

- Traditional databases: For many businesses, tools like MySQL or PostgreSQL are more than enough. They handle data storage efficiently without the added complexity of blockchain.

- Cloud solutions: Platforms like AWS or Microsoft Azure offer scalable, flexible, and cost-effective ways to store and process data. You can customize them to suit your needs without the overhead of managing a blockchain network.

- Other distributed ledger technologies: Blockchain isn’t the only game in town. If privacy and regulation are top concerns, especially in industries like finance or healthcare, a permissioned DLT like Hyperledger Fabric might be a better choice than a permissionless blockchain.

Choosing the right blockchain for your business

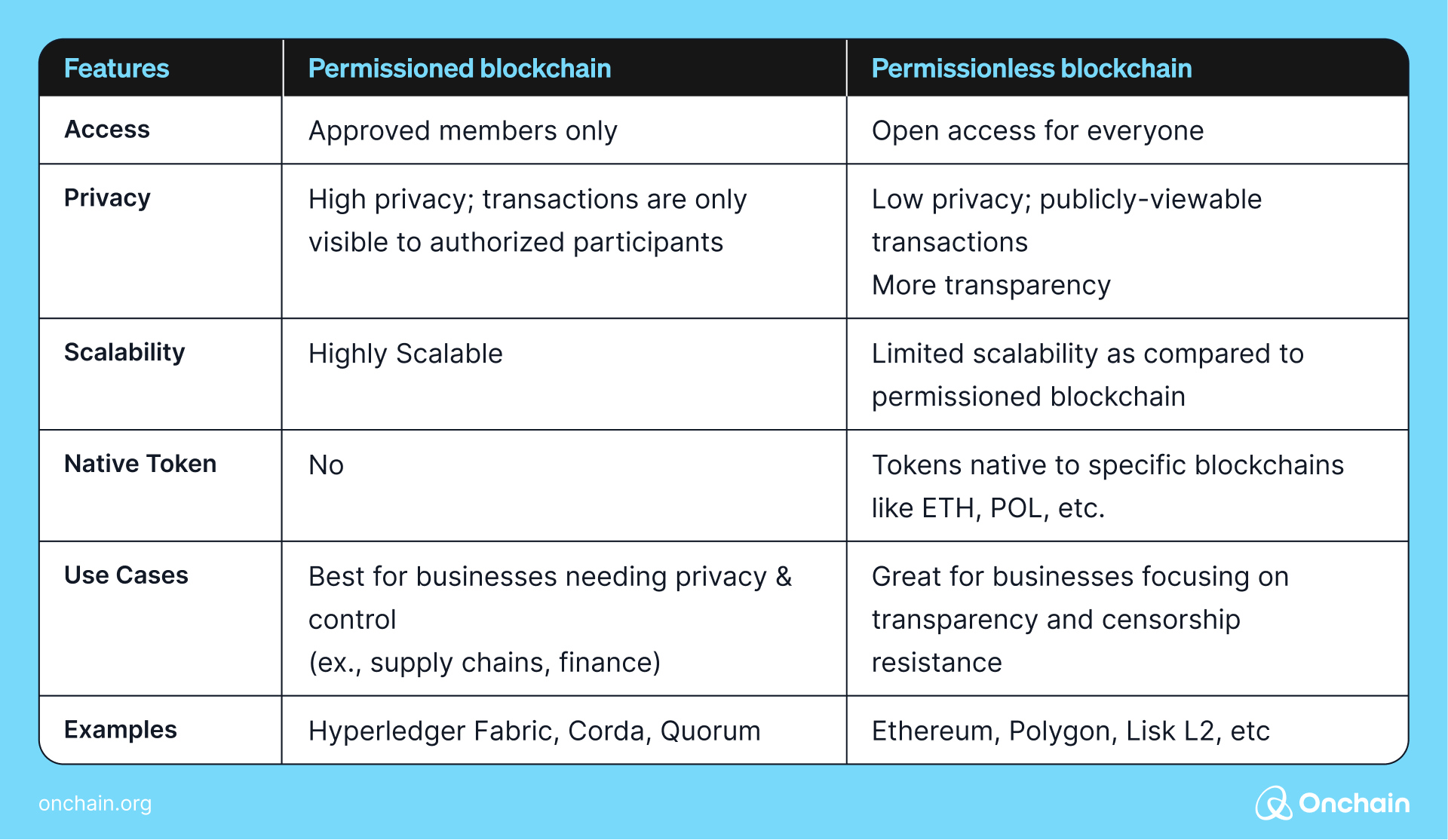

If you determine that blockchain is indeed the right solution, the next step is to choose the type that best suits your needs. Your decision will come down to selecting between permissioned (like Hyperledger Fabric, Corda, Quorum, etc.) and permissionless (like Ethereum, Polygon, Lisk L2, etc.) blockchains, each of which offers distinct advantages.

Hyperledger Fabric was one of the first permissioned blockchains developed by IBM. Its main focus was to design a modular architecture that allows businesses to build customized blockchain networks that precisely address their specific needs and processes.

This flexibility streamlines operations and enhances efficiency, as the platform can be adapted to fit seamlessly within existing infrastructure and workflows. This was evident from one of the giant supply chain companies, Walmart, which was initially a blockchain skeptic but later realized its potential and integrated it into its system.

“I really had an “aha” moment once I deeply understood the technology. I had been hesitant about creating yet another traceability system – the ones we had tried in the past never scaled. Now I understand that was because they were centralized databases. Blockchain, with its decentralized, shared ledge, felt like it was made for the food system!” (source)

– Yianna, Vice President, Food Safety, Walmart

Later, Quorum was specifically designed to address privacy concerns in enterprise blockchain applications. While Corda was designed for interoperability and data privacy, it is particularly suited for applications involving legal contracts and multi-party collaboration.

In essence, permissioned blockchains offer greater control and privacy all within their modularized architecture, making them well-suited for enterprise applications and use cases where sensitive data is involved.

On the other hand, permissionless blockchains like Ethereum, Polygon or Lisk L2 prioritize transparency and censorship resistance, making them ideal for public networks and decentralized applications (dApps).

They embody the core principles of decentralization and openness that define the Web3 vision. For example, a wide range of dApps, including decentralized exchanges, games, and social networks, are built on this vision. Compound, and Uniswap are popular DeFi platforms built on Ethereum.

The blockchain crossroads – a journey of choice

So, is blockchain the golden ticket for your business? Not always. It’s like a powerful tool in your toolbox – perfect for some jobs, overkill for others.

Think of it this way: if you’re building a simple birdhouse, you don’t need a jackhammer. But if you’re constructing a skyscraper, a hammer alone won’t cut it. Similarly, blockchain shines when trust is shaky, multiple hands are on deck, and an unchangeable record is crucial.

Don’t fall for the hype. Explore all your options first. Sometimes, a trusty old database or a cloud solution will do the trick.

Remember, technology is a tool, not a trophy.